")

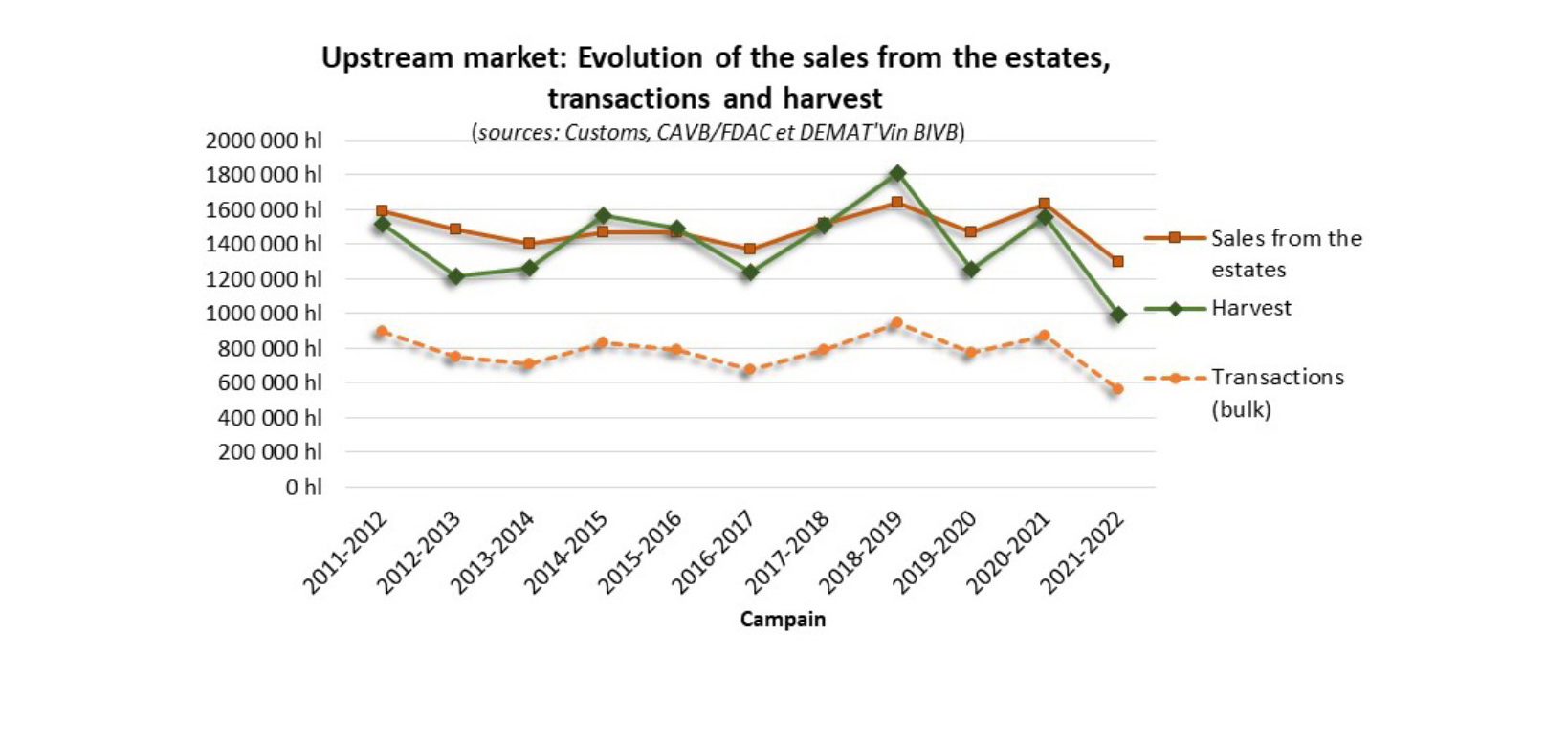

In recent years,yields in Bourgogne varied significantly. If one takes a long-term view, annual production has been falling slowly since2003, with the 2021 vintage only serving to amplify this trend. Fortunately, the 2022 vintage promises to be a generous one, and comes at the right moment to reinvigorate the industry in terms of availability and sales potential.

The small 2021 harvest (around 997,000 hl, or just over 132.9 million bottles) had a big impact on availability and sales from the estate.

While stocks on estates at the end of July 2022 seem to be well below the five-year average, these are supplemented by equivalent stock levels with the négoce trade.

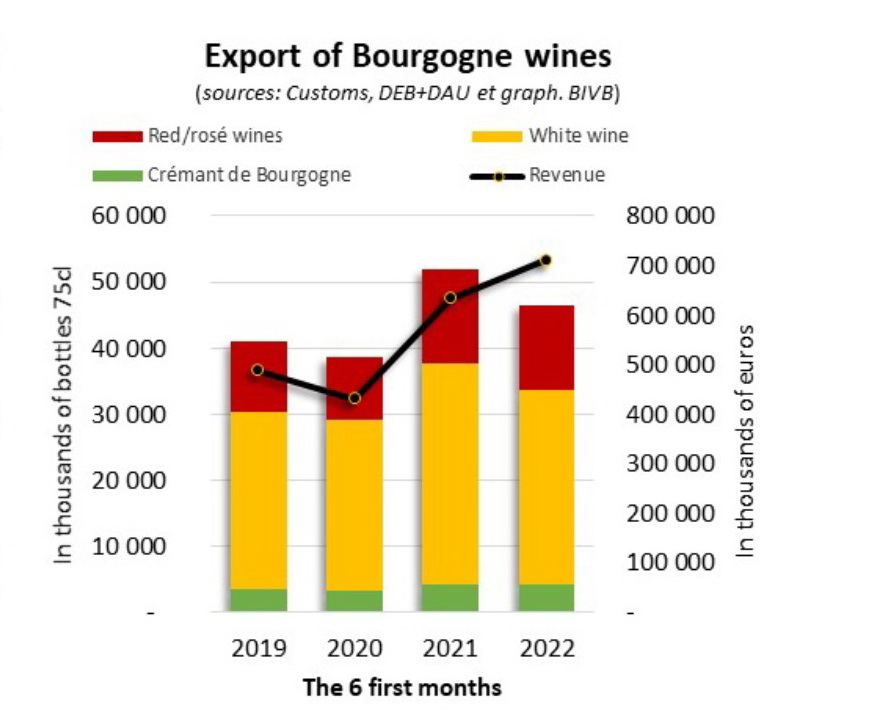

In terms of exports, revenue continues to grow, unlike volumes which, despite everything, remain higher than they were in 2019. They were up 13% by volume for the first six months of 2022 compared to the same period the previous year.

Upstream Market - Sales from the estates shift in pace

When the first figures for the 2021 harvest were announced, markets for Bourgogne wines grew nervous, boosting the number of bottles sold from estates of vintages prior to 2021.

As a result, and despite the historically low volumes of the 2021 harvest (down 30% over the average for the past five harvests), the release of wines from the property (in bulk and in bottles) decreased by 15% compared to the average of the last five campaigns (1.3 million hectoliters for the 2021-2022 campaign).

Bulk transactions for the 2021-2022 campaign, totaling 564,716 hectoliters, were badly affected by the fall in volumes harvested:

- 84% of transaction volumes for the 2021 vintage

- Down 30% in terms of volume for the 2021-2022 campaign compared to the average for the five previous campaigns.

Sales from the property in bottles partially cushionedthe fall in bulk transactionvolumes. These were up 10% for bottle sales during the 2021-2022 campaign compared to the five-year average, accounting for 52% of sales from the property by volume, compared to 40% for the average over the past five campaigns.

Overall, sales from properties for the 2021-2022 campaign accounted for nearly 60% of wines available at the start of the campaign. This proportion is the same as for the 2020-2021 campaign, but 2020-21 had much higher volumes (1.6 million hectoliters). They remain, nonetheless, 10 points higher than the average over the past five years.

- White wines: Sales from the property for 2021-2022 accounted for almost 62% of wine available at the start of the campaign, with 58% being the average over the past five years.

- Red wines: Sales from the property accounted for almost 50% of wine available at the start of the campaign, with 48% being the average over the past five years.

One must go back to the very good 1997-1998 campaign to find comparable figures.

At the end of the 2021-2022 campaign in July 2022, stocks at the property were under the bar of one million hectoliters with almost 900,000 hectoliters; or 14 months of average sales (for the 12 months to the end of July 2022).

- In more detail, the stock by month of sales for the different AOCs in Bourgogne varied from four months for certain white Village AOCs to 35 months for other more prestigious AOCs.

- From November, the 2022 harvest, which looks set to be a generous one, should help build stocks back up at the property.

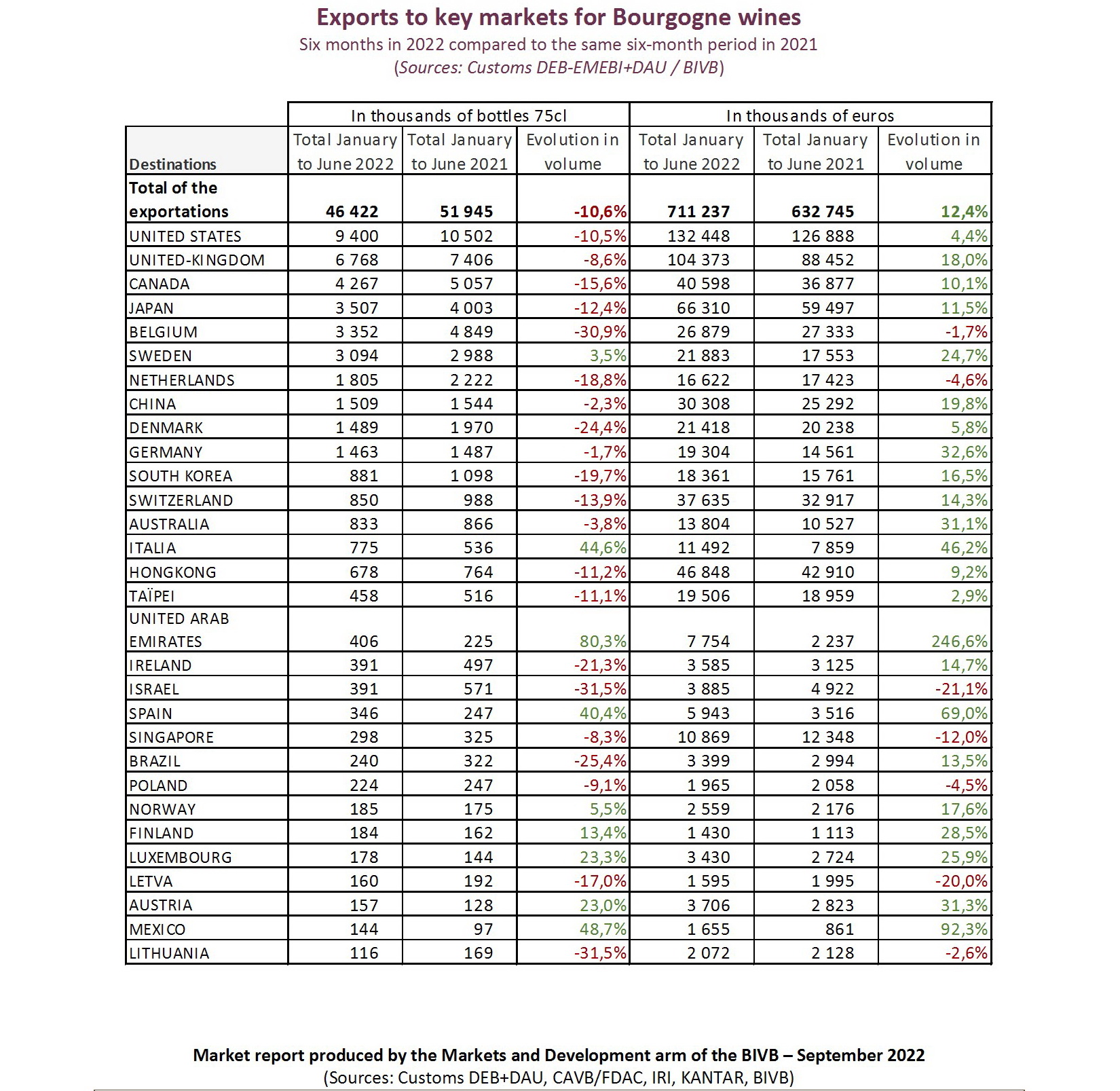

Exports: The availability of Bourgogne wines affects growth by volume, and more

After the boom in sales following various lockdowns and in an economic context filled with incertitude, exports of Bourgogne wines declined, down 10.6% by volume for the first six months of 2022 compared to the same period in 2021. This dip in export volumes, which had a lot to do with the lack of stock, was accompanied by good growth in terms of revenue, which was up 12.4%.

This slowdown came after three record years. Nonetheless, exports remained higher than in pre-Covid times, with 46.4 million bottles exported in H1 2022, up 13% by volume over H1 2019, with an additional 5.3 million bottles being snapped up. These results should be examined in detail, however, because several AOC groups are yet to return to pre-Covid sales levels across a range of key markets.

“This slowdown in exports can be explained by the low yields in 2021,” explains François Labet, President of the BIVB. “Estates and négociants have had to reduce the wine allocated to their various customers in order to satisfy everyone. Stocks are at their lowest and we will have to wait until the 2022 vintage arrives. The volumes we have just harvested, along with a weak euro for our dollar-zone customers, should breathe fresh life into 2023 sales.”

French AOC winegrowing regions also saw a decline, with almost 7.7 million fewer bottles exported in the first half of 2022, down 2% compared to the same period last year. Revenue was more than half a billion euros, up 13.5%. Bourgogne stood up better than any other French AOC region compared to 2019.

Over the past 12 years, the five main markets by volume for Bourgogne wines have remained the same. The USA, UK, Canada, Japan, and Belgium are members what we could call the Famous Five.

Combined, over H1 2022, they accounted for:

- 59% of volumes of Bourgogne wines bottles sold (27 million euros of a total of 46 million euros)

- 52% of export revenues for Bourgogne wines (371 millions euros of a total of 711 millions euros).

These Famous Five have, however, lost some of its market share in Bourgogne wines in H1 2022 compared to H1 2019:

- Export volumes fell from 63% to 59% • Export revenue fell from 56% to 52%

Other markets have seen better growth, slowly chipping away at the Famous Five’s lead:

- This is particularly the case for Sweden, the sixth biggest market by volume for Bourgogne exports. Since 2017, it has seen constant growth, by volume and in terms of revenue. This growth was confirmed by figures for H1 2022, with exports to Sweden up 3.5% by volume and up 24.7% in terms of revenue, compared to H1 2021.

- Other growing markets include the Netherlands, Denmark, and several territories in Asia, such as China, South Korea, Hong Kong, and Taiwan.